Construction is a business of promises made visible in concrete and steel. Between the notice to proceed and the punch list, weather, supply chains, subsurface surprises, and human frailty all conspire to pull parties away from their commitments. Owners want certainty of outcome and schedule; contractors want to manage risk and get paid for the work they actually perform. A performance bond sits in the middle of that tension. Done right, it translates promises into enforceable incentives that narrow the gap between what the owner needs and what the contractor intends to deliver.

I have sat on both sides of that table: writing specs as an owner’s rep on public projects, and later, sweating cash flows as part of a contractor’s project executive team. Performance bonds are nothing like a panacea, yet I have seen them quiet disputes before they start, surface uncomfortable truths early, and keep shaky projects out of court. They do this not by adding more paper, but by shaping incentives in ways that matter when the schedule is slipping and tempers rise.

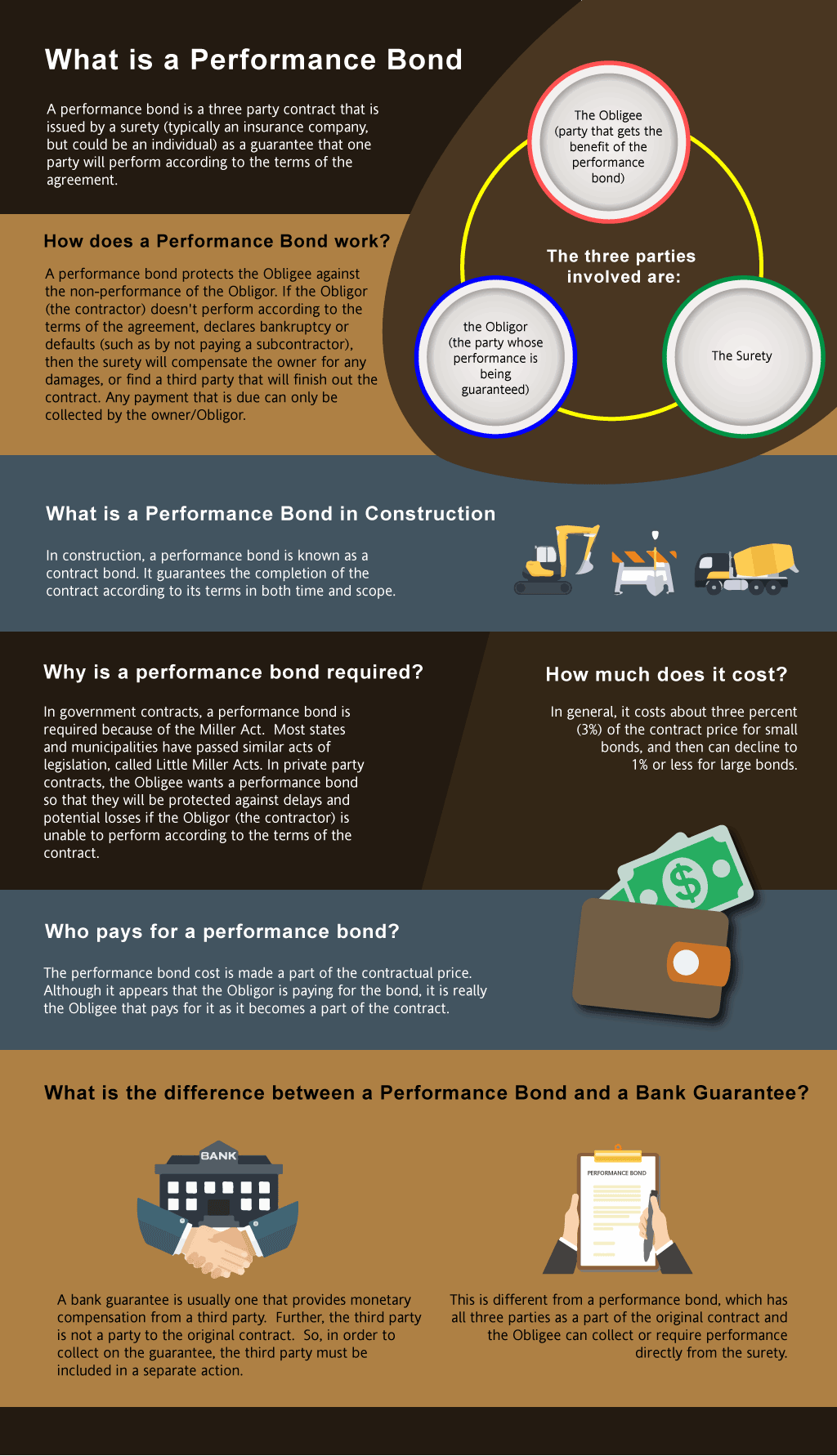

What a Performance Bond Actually Does

Strip away the formal language and a performance bond is a three-party agreement. The owner (obligee) expects the contractor (principal) to fulfill the contract. A surety, typically a specialized arm of an insurer, guarantees that fulfillment up to a stated dollar amount if the contractor defaults. That guarantee is not free money. The contractor indemnifies the surety for any losses, and sureties underwrite bonds using a rigor that blends banking and construction know-how.

If a default occurs and the owner properly declares it, the surety has options written into the bond form. It can finance the original contractor to finish, bring in a completion contractor under a takeover arrangement, tender a replacement contractor the owner accepts, or pay the owner to complete the work, up to the penal sum. The owner does not receive a windfall. The surety also expects cooperation: notice, time to investigate, and a chance to select the remedy.

That mechanism matters for incentives. Everyone at the table knows there is a backstop. The contractor knows a misstep can trigger a surety that has a legal right to take over and a long memory when it comes to future bonding capacity. The owner knows that a default will not leave a half-built shell with only lawsuits to follow. The surety, with skin in the game, has every reason to press for sound project controls before a crisis develops.

Why Owners Want More Than a Signature

Owners, especially public agencies and institutional clients, value predictability. A project that opens a year late erodes public trust, campus planning, and debt service coverage. They also shoulder risks contractors cannot control: user changes, utility conflicts, and discoveries in old buildings. In this mix, a performance bond functions as a hedge against execution failure and a lever to insist on professional behavior.

I once worked with a municipality that had suffered two high-profile project collapses in a decade, both mid-construction. By the time the lawyers finished, the legal fees had burned the equivalent of a new police station. When they required 100 percent performance bonds on subsequent vertical work, they were buying more than payout protection. They were buying the surety’s discipline. We saw cleaner submittal logs, more realistic baseline schedules, and a noticeable drop in change order posturing. Contractors that could not pass underwriting self-selected out during procurement, which spared the city political grief later.

Owners do pay for this. Bond premiums are wrapped into the contractor’s price. Depending on jurisdiction, scope, and contractor financials, the premium for a 100 percent performance bond often falls in a range of roughly 0.5 percent to 2.5 percent of the contract value, sometimes tiered across progress milestones. For a $25 million building, that is a six-figure line item. The calculus is straightforward: is the premium small compared to the cost of failure? On public projects with statutory bonding and on private projects with material revenue risk, the answer is usually yes.

Why Contractors Accept the Scrutiny

From a contractor’s seat, a bond is both a ticket to bid and a set of handcuffs. Securing bonding capacity means opening the books, including personal indemnity from owners and often spouses. It also means living with covenants about working capital, debt levels, and dividend practices. Most contractors accept this because the alternative is worse. Without bonding, large public work is off the table, and many private owners will not award multimillion-dollar contracts without it.

The upside for contractors is subtle but real. The underwriting process, when handled by a competent surety agent, shines a light on the company’s weak spots before they become fatal. I watched a regional general contractor try to stretch from $15 million annual revenue to $60 million in two years. The surety balked, and after some bruising conversations they re-staffed estimating, built a preconstruction group, and added a scheduler with field experience. Growth slowed, then stabilized, and they kept their bond line intact. The premium they paid functioned like a performance coach and a governor on reckless expansion.

Bonding also sharpens internal incentives. Project executives carrying bonded work know that sloppy cost reports and late notices are not mere internal policy violations. They are potential defaults. That understanding tightens discipline around monthly work-in-place, pay application integrity, subcontractor lien releases, and change management. It can be the difference between discovering a bust at 15 percent complete, when options abound, and at 85 percent, when the project is a hostage.

The Surety as Quiet Referee

Owners and contractors both face blind spots. Owners tend to worry early about not getting what they bought, then get distracted by user committees and donor requests. Contractors live in the daily fray of procurement, weather, and manpower, which makes long-horizon risk feel abstract. The surety, whose only product is contingent performance, monitors the horizon. They look for patterns that foreshadow default: negative cash position across jobs, repeated schedule slippages against a baseline with float consumed, erosion in gross margin from buyout to mid-project, or late payments to key subs.

When a wobble shows, sureties do not wait for a formal default. They pick up the phone. I have been in those three-way calls. The surety asks for a plan of correction, not blame. They may require a third-party cost-to-complete analysis, bring in a consultant scheduler, or ask for biweekly reporting instead of monthly. None of that is to please the owner; it is to reduce the odds that the bond is called. But the owner benefits. The presence of a neutral with leverage can pull the discussion from finger pointing to countermeasures.

One case sticks with me. A lab renovation with a compressed shutdown window hit an equipment delivery failure that was no one’s fault. The contractor floated the idea of pushing the turnover date and paying liquidated damages. The owner rejected that outright since the damages would not cover the cost of relocating research. The surety’s analyst joined the meeting, asked penetrating questions about crews and night shifts, then offered to finance overtime for three weeks if the contractor would agree to weekly earned-value reporting and allow a surety-selected superintendent to supplement nights. Pride took a hit, but the project finished inside the shutdown, and the surety avoided a far more expensive default.

How the Bond Realigns Risk Sharing

Construction contracts already assign risk, but paper alone does not control behavior on a live job. Performance bonds add consequences that make parties behave closer to contract intent.

- The contractor’s incentive to finish is sharpened. With indemnity on the line, default is not an exit; it is a financial wound that follows owners personally in closely held firms. That keeps focus on completion, even if profit has evaporated. Many of the hardest-fought completions I have seen were run near cost-only at the end, with contractor leadership on site to protect the company’s bond line. The owner’s incentive to be fair is reinforced. Triggering a bond is not trivial. Sureties will look at whether the owner honored its payment obligations, issued timely decisions, and avoided scope meddling without change orders. Owners who know they may need the surety’s cooperation later tend to keep clean files, give prompt responses, and avoid starving the job of cash as leverage. That improves overall project hygiene. The surety’s incentive to intervene early aligns with both. They prefer a difficult completion to a messy default. Intervention usually means more transparency: real schedules, accurate cost forecasts, and early identification of claims. Owners win because problems surface sooner. Contractors win because they get support that bank lenders rarely understand how to provide on construction risks.

These aligned incentives also change the posture on claims. Without a bond, disputes often drag until closeout, when claim piles collide with withheld retainage. With a bond, the surety often presses for structured claim resolution on the fly. The discipline of contemporaneous documentation and schedule analysis reduces both frivolous claims and owner denial.

Common Misconceptions and What They Cost

A few myths linger around performance bonds and are worth clearing, because they distort expectations and behavior.

The bond is not an all-risk insurance policy for the owner. It does not pay for design defects, owner-caused delays, or scope changes that were never priced. If an owner uses the bond as a cudgel to extract betterment, the surety will either push back or, if forced into payout, pursue recovery via indemnity. I have seen owners lose months thinking the bond would fund redesign work after a late code interpretation blew up a plan. The surety’s polite answer was no.

The bond does not release the contractor from liability. Contractors sometimes imagine that if they lose money, the surety will step in and smooth it over. In reality, any cost the surety pays to complete the project becomes a debt the contractor is obliged to repay under the general indemnity agreement. That agreement often reaches to personal assets. A contractor who rides the surety like a credit card will find future bonding capacity frozen.

The surety will not “just pay the penal sum” at the first sign of trouble. Many owners believe calling the bond is like cashing a check. In practice, the surety investigates carefully. They want to establish whether a default has occurred under the contract terms, whether the owner is in material breach, and what remedy minimizes loss. Attempts to weaponize the bond in a live dispute rarely end well, and they can backfire into prolonged standstill.

Scope Matters: Not Every Project Needs the Same Bond

Owners sometimes ask whether they need a 100 percent performance bond on every job. The answer requires judgment. Statutes settle the question on public work, but in the private market, I weigh three factors.

First, the effect of failure. If non-completion would cripple operations or erode revenue that cannot be recaptured, a full bond makes sense. Acute care hospitals, data centers, major retail openings tied to seasonal calendars, and student housing ready for fall move-in fall into this bucket. These projects do not have soft landings.

Second, contractor profile. An established CM-at-risk with long relationships and a robust balance sheet offers a lower probability of default than a first-time prime on a lump-sum award. But profiles can mislead. I ask to see the contractor’s backlog relative to working capital and net worth. If the new assignment would push them outside the “ten times working capital” rule of thumb many sureties use for capacity, I prefer to let the surety referee with a bond.

Third, delivery method. Under design-build with guaranteed maximum price and transparent open-book accounting, some owners accept a lower bond percentage combined with subcontractor default insurance and joint checks for critical trades. Under hard-bid lump sum with minimal preconstruction integration, I lean to full bonding. The more opaque the price build and the weaker the collaboration history, the more a bond helps.

On small tenant fit-outs or maintenance contracts where the owner can replace a contractor in days without catastrophic loss, a performance bond can be overkill. Other tools, such as retainage, step-in rights to subcontracts, and purchase order assignment, may suffice. The point is not to treat the bond as a ritual, but as a mechanism to align behavior where failure would hurt most.

Pricing and How It Filters Bidders

The headline premium is not the only price. Bidders bake bonding into margins and into the overall posture of risk. A contractor paying 1 percent for performance and payment bonds on a $40 million job must absorb $400,000 before profit. Low-margin bidders who cannot comfortably carry that will either pass or try to make it up elsewhere, often in change orders. Good specifications and clear addenda reduce that temptation, but incentives still bite. Owners who require bonds should invest in scoping clarity and decision speed to avoid squeezing contractors into a corner where they must hunt margins in claims.

Bond requirements also filter the field. On a courthouse project I supported, the bonding requirement shrank the bidder pool from eight to three. Some owners panic at the reduced “competition.” What we actually saw was elimination of undercapitalized firms that would have been dangerous winners. The three who remained had stable EMR ratings, established banking relationships, and stable leadership teams. The bids were within two percent of each other, and the project finished two months early with minimal disputes. The filtering worked as intended.

How Bonds Shape Day-to-Day Project Behavior

Alignment is not only about default. It shows up in decisions made in trailer meetings and procurement calls.

Schedule realism. Because the surety scrutinizes baseline and updates when trouble brews, contractors bonded on tight jobs often privilege credible logic over rosy dates. In one airport gate expansion, the contractor pushed back on an owner-driven requirement to compress the steel sequence by three weeks. They cited float erosion and weekend crane limits at the airside. The surety quietly backed them. The owner relented, and the sequence held. That single decision likely saved a claim months later.

Subcontractor selection. Contractors who know the surety will ask questions about key trades tend to avoid rolling the dice on unproven sub low bids. They go with best value and capacity. On a bonded hospital job, the general contractor bypassed a plumbing sub who was two percent low because their backlog had doubled in six months. The surety’s prequalification tool flagged the growth risk. The slightly higher award avoided a change order flood later when the sub would have run thin.

Change management. The presence of a bond nudges owners to decide and contractors to document. Photographs, daily reports, dated RFIs tied to schedule fragnets, and cost backup accumulate with cleaner chain of custody. The reason is not romance with paperwork. It is that everybody knows the surety may review the file if money or time get tight. That shared awareness improves the quality of the record.

Cash discipline. Bonds ride alongside payment bonds in most jurisdictions. That pairing makes slow pay to subs dangerous. Contractors prioritize pay applications, lien waivers, and timely disbursements because they do not want the surety fielding calls from unpaid trades. Owners benefit because healthy subs are the ones who show up tomorrow with manpower.

When Bonds Do Not Prevent Pain

A bond is a safety net, not a parachute. It does not eliminate all bad outcomes, and it can introduce its own friction.

Time is the first casualty in a bond-triggered remedy. If the surety needs weeks to investigate a potential default while a project idles, the schedule may stretch beyond what money can cure. Owners who must meet immovable dates can bite their lip watching that clock. Some mitigate with interim agreements that allow partial surety financing while facts are sorted, but those are negotiated under pressure.

Scope clarity is the second. If drawings are 70 percent complete at award and design continues deep into construction, aligning what exactly must be performed under the bond takes lawyering. Target value design and progressive GMPs offer owner flexibility, but the more fluid the scope, the harder it is to define a clear contractor default that a surety will accept. You can still bond such projects, but expect more attention from the surety on scope control and change authorization.

The third is contractor morale. The presence of a surety-appointed consultant on site can feel like an audit. Some teams bristle. Communication helps. When I have walked into those rooms as an outside advisor, I start by making it clear I work for the surety to prevent a default, not to find fault, and I show the fastest path to finish without trivia. That usually diffuses egos.

Practical Steps to Make the Bond Work For, Not Against, the Project

- Choose the right bond form and align it to your contract. Standard forms like AIA A312 are well understood. Modify only with counsel, and keep remedies and notice periods workable. Prequalify deeply and coordinate with the surety early. Owners who call the surety agent during procurement, with the contractor’s consent, learn more about capacity and recent performance than any glossy proposal will show. Tie scheduling rigor to bonding expectations. Require a critical path method schedule with monthly updates and fragnet analysis for delay events. If the project is fast-track, insist on weekly updates during critical sequences. Maintain discipline on payment and decisions. Owners who starve a job or drag on submittals hand contractors excuses and give sureties reasons to push back later. Pay what is due, when due, and answer RFIs promptly. Build positive relationships before trouble shows. Regular three-way check-ins among owner, contractor, and surety agent, even if brief, create a shared picture. In a crunch, that trust speeds solutions.

These five moves reinforce the alignment the bond intends to create. They do not require heroics, just steady management.

A Short Case Study: Two Jobs, Two Outcomes

Two midsize wastewater plant upgrades started six months apart in neighboring counties, each around $30 million. One owner required full performance and payment bonds with AIA A312 forms, plus monthly CPM updates. The other decided to save money by waiving bonds for a contractor with whom they had a friendly history, relying instead on 10 percent retainage and a personal guarantee.

Project A hit a subsurface conflict with an unrecorded duct bank. The schedule cracked. The contractor’s cost reports started showing margin erosion. The surety noticed float consumption and convened a meeting. They financed an additional excavation crew for six weeks and required two-week look-ahead meetings with minutes shared to all. The owner paid timely on undisputed work and approved a change order for the duct bank relocation in two days. The job finished three weeks late, inside the owner’s operational cushion, and liquidated damages were waived under a negotiated settlement based on contemporaneous schedule analysis. No lawyers.

Project B lost its electrical sub, who walked after not being paid for two months. The GC had overbilled on other jobs to cover a separate disaster and was using new billings to pay old costs. Without a surety to call, the owner issued a notice to cure, then terminated. Finding a replacement prime took three months, and the replacement insisted on re-buying major equipment with price escalation that crushed the budget. The personal guarantee turned into a bitter, drawn-out negotiation. The plant upgrade finished two years after the original date, well after the consent decree deadline, and the county paid fines that dwarfed the saved bond premiums.

These two outcomes are not flukes. They reflect how the presence of a performance bond changes behavior and options before and during trouble.

The Human Element Behind the Paper

Contracts and bonds can look like abstractions until you stand in a muddy laydown Home page yard at 6 a.m., watching a foreman radio for a missing bucket while the owner’s rep checks off a day that the schedule cannot spare. What aligns incentives is not magic language. It is a set of credible consequences and supports that nudge people to do the right hard things when nobody is looking.

Contractors work differently when they know a surety analyst will read their cost-to-complete and a claims consultant may scrutinize their time impact analysis. Owners act differently when they know an independent party who understands construction will examine their change directives and pay history before honoring a default. And sureties act differently when they know their own capital is exposed if early problems fester.

Performance bonds are not about mistrust. They are about realism. They accept that even competent teams can be knocked off balance, and they install a mechanism that, most of the time, pulls them upright before they fall. Used thoughtfully, they align owner and contractor incentives around the one goal that matters most on any project: finish what you promised, as close as possible to the day and the dollar you said you would.